What Is Adjusted EBITDA in a Dental Practice Sale — and Why Every Add-Back Is Worth Seven Times Its Value

Apr 17, 2026

If you've received a letter of intent from a DSO, you've seen the term EBITDA. You may have nodded along as your broker explained it. You may have accepted the number your accountant produced without fully understanding how it was derived.

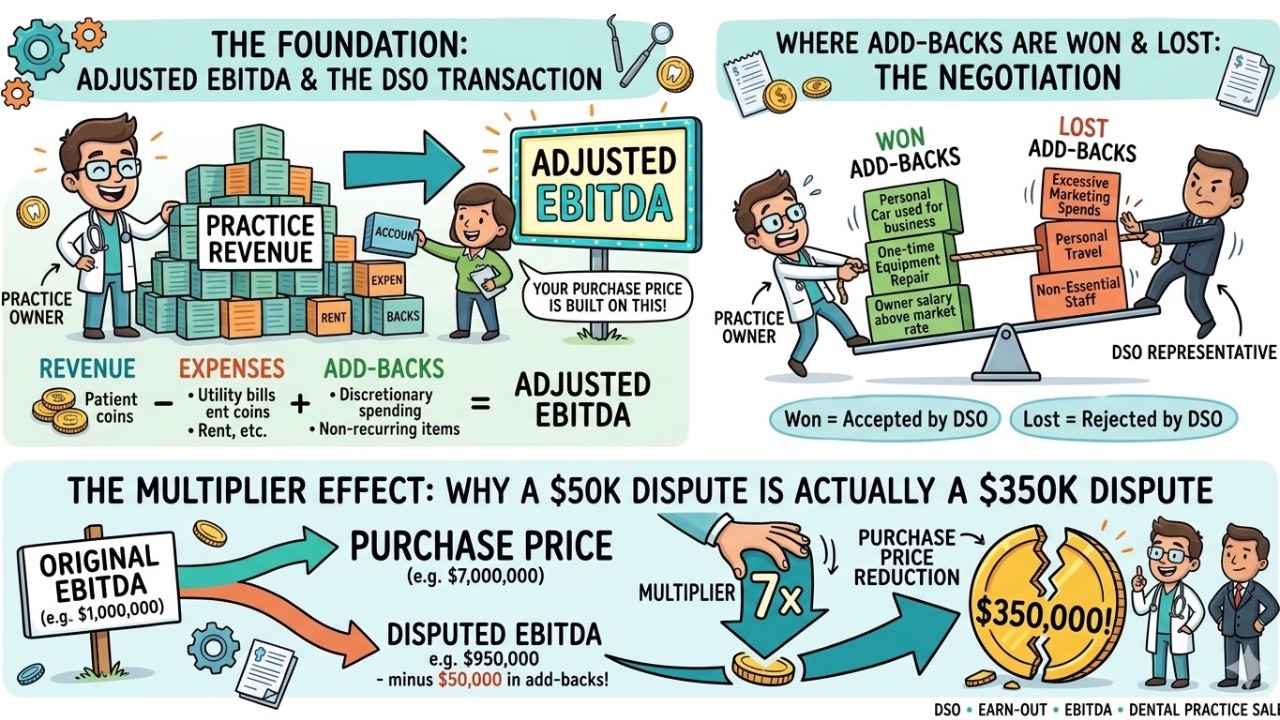

This matters more than almost anything else in your transaction, because EBITDA is the foundation of your purchase price. Every dollar of EBITDA difference multiplies by your deal multiple. In a seven-times deal, a $50,000 EBITDA dispute is a $350,000 purchase price difference. That math is not theoretical. It is real money, at every closing table.

This post explains adjusted EBITDA in plain language — what it is, how it's calculated, which add-backs are accepted and which get challenged, and what you can do before due diligence begins to protect your position.

What EBITDA Is

EBITDA stands for Earnings Before Interest, Taxes, Depreciation, and Amortization. It is a measure of your practice's operating profitability — what the business earns from its operations, stripped of the effects of how you've financed it, structured it, or depreciated its assets.

A practice that generates $2.1 million in collections, has $1.3 million in operating expenses, $80,000 in depreciation, $45,000 in interest on equipment loans, and $175,000 in taxes paid by the entity has an EBITDA of approximately $795,000 before add-backs — roughly ($2.1M - $1.3M) + $80K + $45K.

The add-backs are where it gets interesting.

What "Adjusted" Means

Adjusted EBITDA goes further than base EBITDA by adding back expenses that are specific to your ownership of the practice and would not exist under third-party ownership. The logic is sound: if you paid yourself a salary of $600,000 and a market-rate associate dentist would cost $260,000 to replace your clinical production, the $340,000 difference is an owner-specific expense that inflates your costs artificially. It should be added back to produce a normalized earnings figure.

This adjusted number — base EBITDA plus your add-backs — is what the buyer multiplies by the deal multiple to arrive at your purchase price.

At seven times, $795,000 in base EBITDA produces a $5.565 million purchase price. Add back $340,000 in owner compensation and $75,000 in other accepted add-backs, and the adjusted EBITDA is $1.21 million — producing an $8.47 million purchase price. The add-backs didn't change your practice. They changed your purchase price by $2.9 million.

This is why the EBITDA add-back negotiation is the most important financial conversation in any DSO transaction, and why the buyer's accounting team will scrutinize every single add-back you claim.

The Add-Back Categories That Matter

Owner compensation is the largest and most universally accepted add-back. If you paid yourself above what a comparable associate dentist would earn, the difference is added back. The calculation requires a market compensation analysis — a documented comparison of your compensation to market rate for a dentist of your production level in your market. This analysis should be commissioned before due diligence begins, not after the buyer's team arrives with their own number.

Personal expenses run through the practice are accepted with documentation. Vehicles, club memberships, personal insurance premiums, cell phones used primarily for personal purposes — all are legitimate add-backs when supported by records that establish the personal nature of the expense. The buyer's QoE team will request documentation for each one.

One-time non-recurring expenses are accepted when they are genuinely non-recurring. A major piece of equipment that needed emergency replacement after a failure, a litigation settlement, a facility repair following an unusual event — these are reasonable add-backs. The buyer's team will look at multiple years of financials to test whether expenses characterized as non-recurring actually are. If the same category appears in two of three years, expect a challenge.

Related-party transactions require specific documentation. If you own the building your practice occupies and charge rent to the practice at above-market rates, the above-market portion is an add-back. If you have management fee arrangements with related entities, those are reviewed carefully. The buyer needs evidence that the adjustment reflects reality, not financial engineering.

The Add-Backs That Get Rejected

Planned future expenses are not add-backs, and buyers are consistent and correct in rejecting them. If you are planning to hire an associate dentist and want to add back the anticipated cost as though it doesn't exist, the buyer's response will be that the cost is real and will exist in their hands as well. Forward-looking add-backs are almost never accepted.

Standard recurring expenses that would continue under new ownership — accounting fees, legal fees at normal levels, reasonable marketing spend, technology costs — are not add-backs. They represent the genuine cost structure of the business.

Non-arms-length compensation to family members at above-market rates is partially accepted — the above-market portion is the add-back, not the full compensation. If your spouse works in the practice in an administrative role and is paid $95,000 for duties that a market hire would perform at $58,000, the $37,000 difference is the add-back.

The Quality of Earnings Problem

Here is the dynamic that most dentists don't understand until it's too late.

When the buyer sends their due diligence team, one of the first things that arrives is their Quality of Earnings accountant — a firm whose mandate is to reconstruct your adjusted EBITDA from your financial records and normalize it in a way that is favorable to the buyer. This is not a neutral process. The QoE team is specifically looking for reasons to restate your EBITDA downward: challenging add-backs, identifying overlooked liabilities, applying conservative assumptions to uncertain items.

If you have not commissioned your own independent QoE analysis — ideally before the LOI is signed — you are arriving at this negotiation with no documented position of your own. The buyer's restated EBITDA becomes the starting point for discussion by default. You are defending rather than anchoring.

When you have your own QoE, your number is an established, documented fact. The buyer's team must dispute your analysis rather than constructing a narrative from scratch. This shift in negotiating posture consistently produces better add-back outcomes — typically by amounts that dwarf the cost of the QoE engagement.

The cost of an independent QoE for a single-practice transaction typically runs $15,000 to $35,000. The purchase price protection it provides is routinely worth ten to twenty times that amount.

What the Buyer Is Actually Doing

It helps to understand the buyer's incentives clearly. The DSO's acquisition model is built on paying the lowest defensible price for the highest-quality practices. Their QoE team is not adversarial in a personal sense — they are doing their jobs, which is to normalize your earnings in the way that supports the most favorable purchase price for their client.

Every dollar of your EBITDA they restate downward reduces their cost by the deal multiple. A $50,000 successful add-back challenge costs them $350,000 at seven times. They have significant financial incentive to challenge every add-back that is imperfectly documented or commercially ambiguous.

This is not a reason to distrust the DSO. It is a reason to arrive with documentation.

Before Due Diligence Begins

The practical steps that protect your EBITDA position are straightforward and front-loaded — they need to happen before the buyer's team arrives.

Commission your own QoE before the LOI is signed. Your number becomes the anchor.

Prepare an add-back defense file. For every add-back you intend to claim, one page: description of the add-back, annual dollar amount, documentation supporting it, and the logic for why it is owner-specific and non-recurring. The buyer's team will ask for exactly this information — having it ready before they ask signals preparation and supports your number.

Lock the EBITDA definition into the LOI. Push to include a reference to your add-back schedule in the LOI itself rather than deferring the definition to the APA negotiation. Anything not established in the LOI is negotiated during due diligence, when your leverage has dropped significantly.

Understanding adjusted EBITDA and the add-back negotiation is the financial foundation of any DSO transaction. The full framework — including the Purchase Price Impact Calculator that shows you exactly what each add-back is worth in purchase price terms — is covered in Chapter Two of The Earn-Out Trap and in the 8-Tab Calculator Suite.

Both are available at the link below. The free introductory course covers the EBITDA fundamentals in the first thirty minutes — start there if you want the foundation before you go deeper.

Stay connected with news, offers and updates!

Join our mailing list to receive the latest news, offers and updates from our team.

Don't worry, your information will not be shared.

We hate SPAM. We will never sell your information, for any reason.