The RAP Plan Panic: What Every Dental Student Needs to Know Before July 1

Apr 17, 2026

You've heard it. Or you're about to. Someone in your class drops the phrase "RAP plan" and suddenly the whole table goes quiet. Because nobody really knows what it means, and everybody's scared to admit it.

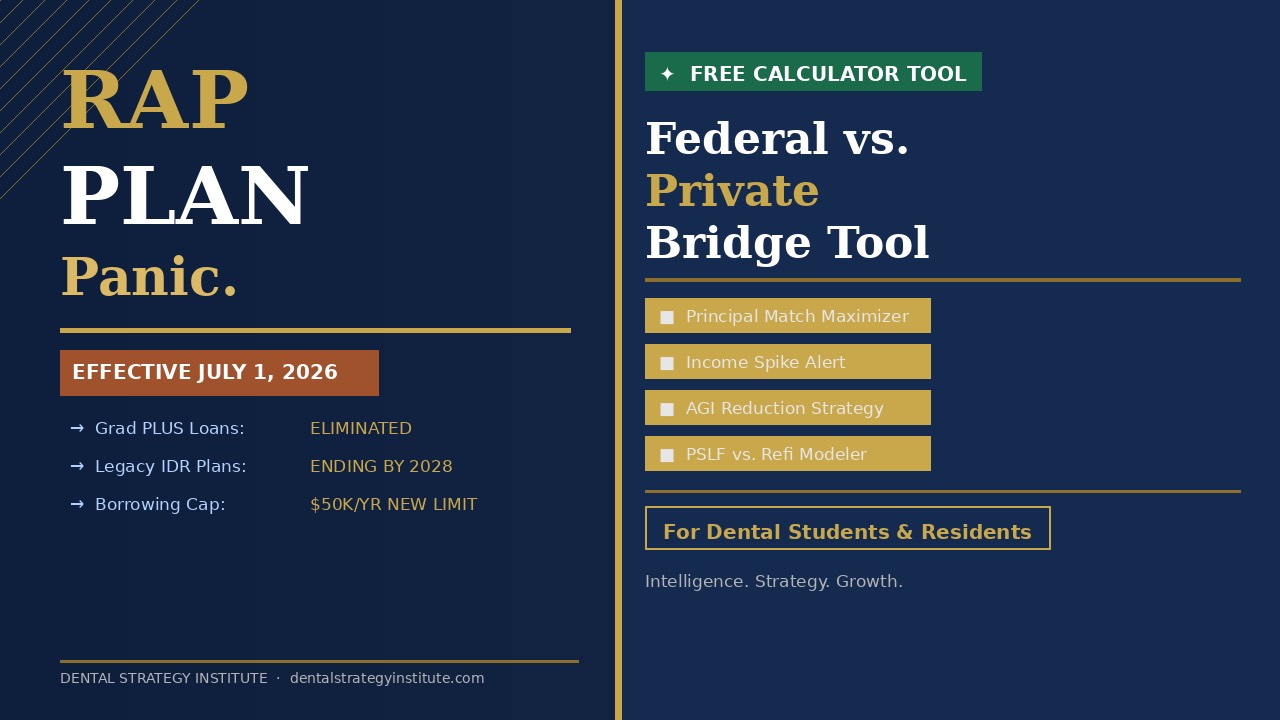

July 1, 2026 changes everything about how dental students borrow and repay federal loans. Grad PLUS is gone. The income-driven repayment plans you've been counting on are mostly dead or dying. And what's replacing them — the Repayment Assistance Plan, or RAP — is generating more confusion than clarity, because most of the articles explaining it are written for English teachers making $48,000 a year, not dental students sitting on $280,000 in debt.

First, What Actually Changed

The One Big Beautiful Bill Act, signed July 4, 2025, blew up the federal student loan repayment system as we knew it. SAVE is gone — killed by the courts in March 2026 and then buried by statute. PAYE and ICR survive until July 1, 2028, then they're gone too. IBR lives on, but only for existing borrowers who don't take out a single new federal loan after July 1, 2026. And Grad PLUS — the loan that let dental students borrow up to the full cost of attendance — is eliminated for new borrowers as of today.

That last part is the one that stings hardest. New dental students are now capped at $50,000 per year in federal borrowing under what the Department of Education calls the "professional student" classification — with a $200,000 lifetime aggregate limit. When the average dental school runs $70,000 to $90,000 per year all-in, that gap has to come from somewhere. Private lenders are going to have a very good year.

RAP: The Good, The Ugly, and the Threshold Problem

Here's how RAP actually works. Your monthly payment is a percentage of your Adjusted Gross Income, graduated across eleven brackets from 1% to a cap of 10% for anyone earning above $100,000. The minimum is $10 per month if you're earning under $10,000. Each dependent child knocks $50 off your monthly payment.

The two features that matter most — and that nobody's explaining clearly — are the interest subsidy and the principal match.

The interest subsidy means that if your payment doesn't fully cover the interest accruing that month, the government eats the difference. Your balance can't grow through negative amortization under RAP. That's genuinely protective and it's the same protection that SAVE offered.

The principal match is RAP's one new trick. If your monthly payment doesn't reduce your loan principal by at least $50, the government applies up to $50 toward your principal automatically. This matters during residency and early associateship years when your income is still modest and your payment barely dents the balance.

Here's the catch that nobody talks about plainly: that $50 principal match only activates when your payment covers less than $50 toward principal. Once your income rises enough that your payment naturally exceeds that threshold, the subsidy disappears. For a dental graduate making $100,000 with $250,000 in debt at 7%, your required RAP payment might be jumping to $833/month — and none of that principal match applies anymore. The subsidy evaporated the moment you crossed the bracket.

This is the "payment spike" problem. When your income crosses from one AGI bracket to the next — say from $90,000 to $100,001 — your required payment percentage jumps by a full percentage point applied to your entire income, not just the dollars above the threshold. That's the mechanism that catches people flat-footed at their first income recertification.

The Private vs. Federal Decision

Here's where it gets complicated for dental students entering in 2026 and beyond. With Grad PLUS gone and a $50,000 annual federal cap, many of you will need to fill a $30,000 to $50,000 annual gap with private loans. And private loans play by completely different rules.

Private loans offer lower headline interest rates — sometimes meaningfully lower than the federal rate, which has been hovering in the 7%–8% range for graduate borrowers. But private loans carry no PSLF eligibility, no income-driven repayment protection, and no government subsidy of any kind. If your income craters during a health crisis or a practice transition, private loans don't care.

The core question is whether you're planning to pursue Public Service Loan Forgiveness. If you are — and you're working toward a qualifying nonprofit or government employer for ten years — then protecting your federal loan balance for PSLF makes RAP a strong choice. Higher RAP payments still count as qualifying payments, and after 120 of them, whatever's left is forgiven.

If you're going straight into private practice, the math shifts. Private refinancing of federal loans gives you access to potentially lower rates and a fixed repayment window, but you permanently forfeit every federal protection including RAP, PSLF, and the interest subsidy. That's not a trivial trade.

Three Numbers You Should Know Cold

The RAP bracket that applies to you is based on your prior year's AGI — not your current income. This matters because if you're in a low-income residency year and you recertify on time, your payment stays low even as you start your first year of associateship. But the moment you recertify after your first full income year as an associate, your payment jumps to match the new bracket.

Your AGI is manageable. Pre-tax retirement contributions (401k, SEP-IRA), HSA contributions, and student loan interest deductions all reduce your AGI before RAP calculates your payment. A new associate maxing a 401k at $24,500 drops their AGI by that amount — which at the 8% bracket translates to roughly $163 per month in payment savings. That's real money.

And the 30-year forgiveness clock starts when you enter repayment — not when you graduate. Don't conflate your graduation date with your repayment start date. They're often separated by a grace period, a residency deferment, or a period of economic hardship forbearance, and each of those affects your clock differently.

What to Do Right Now

If you already have federal loans and aren't taking out new loans after July 1, you may have more flexibility than you think. Check your current plan — if you're in PAYE or ICR, you have until July 1, 2028 to transition to either IBR or RAP. Don't sit on autopilot and get auto-enrolled; run the numbers first.

If you're starting dental school now or in the next cycle, build your full four-year cost model before you borrow a dollar. Know exactly how much federal borrowing covers, how much private borrowing fills the gap, and at what income level RAP's payment becomes more expensive than a private refi. That calculation changes significantly depending on whether you're PSLF-eligible.

We built the RAP Bridge Calculator specifically for this decision. It's free. Use it.

Access the FREE RAP Plan Calculator Now

This content is for educational purposes only and does not constitute financial or legal advice. Loan terms and federal regulations are subject to change. Consult a qualified student loan advisor for guidance specific to your situation.

© 2026 Dental Strategy Institute. All rights reserved. | dentalstrategyinstitute.com

Stay connected with news, offers and updates!

Join our mailing list to receive the latest news, offers and updates from our team.

Don't worry, your information will not be shared.

We hate SPAM. We will never sell your information, for any reason.