The SEP IRA: The Highest-Limit Retirement Plan Most Dental Practice Owners Aren't Using Correctly

Jun 08, 2026

By Dental Strategy Institute | June 2026 | 8-Minute Read

If you are a dental practice owner and you are not maximizing a retirement plan designed specifically for business owners, you are paying more in taxes than you need to. There is no more accurate way to say it.

The SEP IRA—Simplified Employee Pension Individual Retirement Account—allows a dental practice owner to contribute up to $72,000 in 2026 to a tax-deferred retirement account. That contribution is fully deductible as a business expense. It requires no annual IRS filing, no plan testing, no third-party administrator, and can be established on a single two-page IRS form.

Most dentists know it exists. Far fewer are using it to its full potential—and even fewer understand the one rule that can make it expensive if you do not plan for it correctly.

This article covers both.

What Makes the SEP IRA Different

There are five qualified retirement plan options commonly available to a dental practice owner: the SEP IRA, the SIMPLE IRA, the Solo 401(k), the traditional 401(k), and the defined benefit plan. The SEP IRA sits at a unique intersection of high limits and low complexity that no other plan matches for the right practice structure.

| Feature | SEP IRA | SIMPLE IRA | Solo 401(k) | Trad. 401(k) | |---|---|---|---|---| | 2026 Contribution Limit | $72,000 | $16,500 | $70,000* | $70,000 | | Employee Contributions? | No | Yes | Yes (solo) | Yes | | Required Employer Match? | No | Yes (2–3%) | No | No | | Catch-Up Age 50+? | No | $3,500 | $7,500 | $7,500 | | Annual IRS Filing? | No | No | Yes | Yes | | Plan Testing Required? | No | No | Yes | Yes | | Setup Complexity | Very Low | Low | Medium | High | | Flexible Year-to-Year? | Yes — optional | Required | Discretionary | Varies |

Solo 401(k) limit combines employee deferral + employer profit-sharing. Source: IRS Notice 2025-67; Kiplinger (April 2026)

The Number That Changes Everything: $72,000

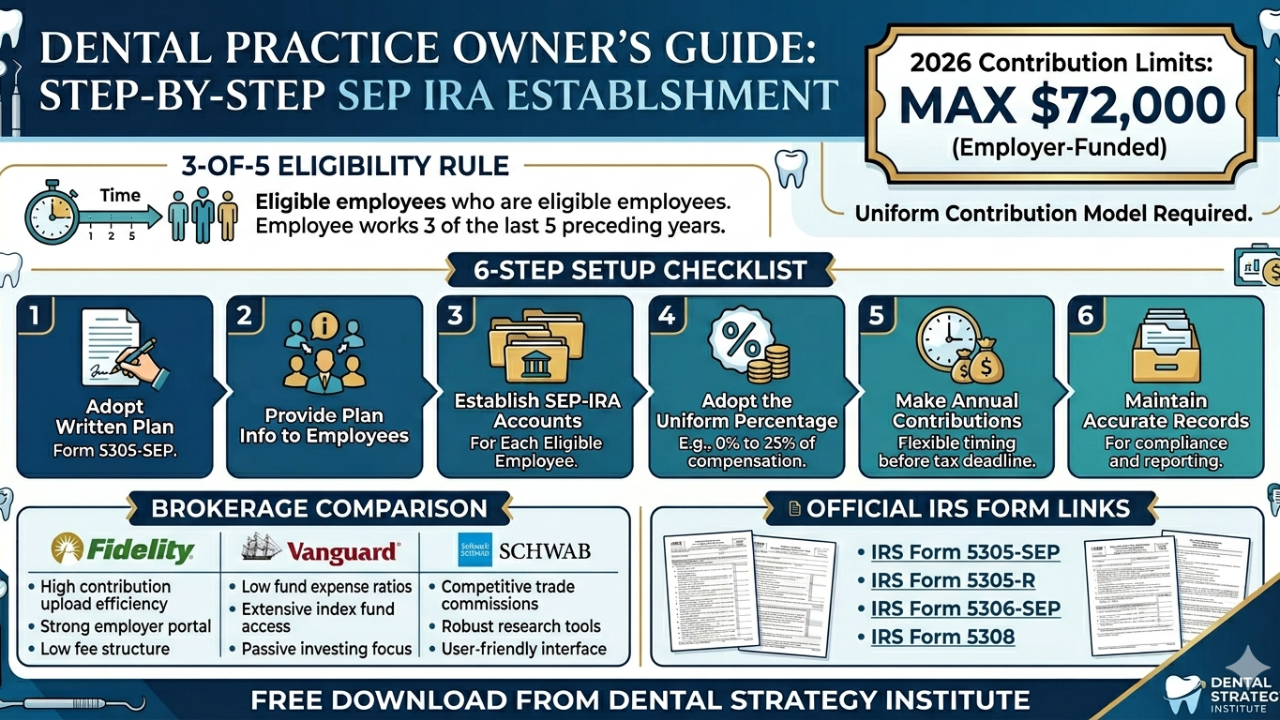

In 2026, the maximum SEP IRA contribution is $72,000 per participant — up from $70,000 in 2025. The formula: up to 25% of each eligible participant's compensation, capped at $72,000. Only the first $360,000 of compensation counts.

For context: the standard Roth or traditional IRA limit in 2026 is $7,500. The SEP IRA limit is nearly ten times higher. For a practice owner in the 32% marginal bracket who maximizes a $72,000 contribution, the immediate federal tax savings is $23,040—in a single year.

The contribution is optional every year. In a strong production year, you fund it to the maximum. In a lean year, you skip it entirely. No plan amendment. No penalties. No compliance event.

KEY INSIGHT: The SEP IRA contribution deadline is your business tax filing deadline—not December 31. If you file on extension, you have until October 15, 2027 to fund a 2026 SEP IRA. You can even establish the plan retroactively up to that same deadline. No other qualified plan offers this setup window.

The One Rule That Can Make It Expensive: Uniform Contributions

Whatever percentage of compensation you contribute for yourself, you must contribute the same percentage for every eligible employee.

If you contribute 25% of your $280,000 compensation — $70,000 for yourself — you must also contribute 25% of each eligible employee's compensation:

- Dental hygienist earning $78,000 → $19,500

- Dental assistant earning $46,000 → $11,500

- Front desk coordinator earning $42,000 → $10,500

Your $70,000 personal contribution comes with $41,500 in mandatory staff contributions. Total employer cost: $111,500. After tax deduction at 32%, the net cost is approximately $75,820 — and you have sheltered $111,500 from federal tax while funding meaningful retirement benefits for your team.

The math works. But you need to run it before you set your contribution rate.

CAUTION: Employee eligibility is determined by the 3-of-5 rule: an employee who worked for you during any part of at least 3 of the last 5 calendar years AND earned $800+ in 2026 must be included. This catches part-time staff, seasonal employees, and returning former employees. Have your dental CPA audit your eligible employee list before establishing or funding the plan.

Who the SEP IRA Is Built For in Dentistry

The Solo Practitioner. No employees means the uniform contribution rule is irrelevant. One form, one account, $72,000 deducted. The simplest path to maximum retirement savings available anywhere.

The Associate-Heavy Practice. If your dental associates are independent contractors, they are not covered by your SEP IRA. Only W-2 employees who meet the eligibility criteria must be included — but confirm contractor classification carefully with employment counsel.

The New Practice Owner. Variable income in the early years makes the optional contribution feature particularly valuable. Contribute aggressively in good years, skip in lean ones.

The Established Owner Approaching Retirement. The SEP IRA delivers the highest annual contribution of any simple plan — but note the absence of catch-up contributions. Owners over 50 should compare directly to a Solo 401(k) with their financial advisor.

Setting Up a SEP IRA: What It Actually Takes

- Download IRS Form 5305-SEP from IRS.gov. Two pages.

- Fill in your business name, EIN, and eligibility provisions.

- Open an employer SEP IRA account at Fidelity, Vanguard, or Schwab — all three at zero setup cost.

- Provide each eligible employee enrollment materials to open their individual SEP IRA accounts.

- Contribute by your tax filing deadline. Wire or ACH directly to each account.

- Repeat annually — recalculate eligibility, decide your rate, fund by deadline.

No administrator. No testing. No annual filing.

Common Mistakes to Avoid

- Skipping the eligible employee audit. The 3-of-5 rule catches staff you may not expect.

- Setting the rate before modeling staff cost. A 25% rate feels right until you apply it to five employees. Model it first.

- Confusing the deadline with December 31. Your deadline is your tax filing deadline including extensions.

- Failing to provide employees with plan documentation. You must give eligible employees a copy of Form 5305-SEP or written notice of their rights.

- Thinking the SEP IRA conflicts with a Roth IRA. It does not. Employees can contribute to a personal Roth or traditional IRA in addition to a SEP IRA, subject to income limits.

📋 Free Tool: DSI SEP IRA Setup Checklist for Dental Practice Owners

A print-ready guide covering the 6-step setup process, 2026 contribution limits, the uniform contribution cost model, the 3-of-5 eligibility rule, brokerage comparison, and all official IRS links.

No cost. Takes 30 seconds. Everything you need to walk into your CPA conversation prepared.

The Bottom Line

The SEP IRA combines the highest contribution limit of any simple retirement plan, full tax deductibility, optional annual contributions, and administrative requirements that amount to a two-page form and an annual funding decision.

The uniform contribution rule is the one meaningful constraint. For solo practitioners, it is irrelevant. For practices with staff, it is manageable with proper planning — and the employee contributions it requires also serve as genuine retention benefits.

If you have not established a SEP IRA and reviewed your contribution strategy with your dental CPA this year, that conversation should be scheduled this week.

→ Download the Free SEP IRA Setup Checklist

Official Resources

- IRS Form 5305-SEP

- IRS SEP Plan FAQs

- IRS Publication 560 — Retirement Plans for Small Business

- IRS SEP Contribution Limits

- Fidelity SEP IRA

- Vanguard SEP IRA

- Charles Schwab SEP IRA

© 2026 Dental Strategy Institute. All rights reserved. | dentalstrategyinstitute.com

Stay connected with news, offers and updates!

Join our mailing list to receive the latest news, offers and updates from our team.

Don't worry, your information will not be shared.

We hate SPAM. We will never sell your information, for any reason.